Private Markets Are Going Core

Welcome to The Smart Portfolio, where each week, we share the best wealth-building ideas from investing podcasts, hedge fund letters, and interviews with wealth builders

In this issue:

How Franklin Templeton thinks about private markets for wealth clients in 2026

Email tactics that engage clients: stop educating, your goal is to communicate that you understand your clients on a deeper level

This advisor started charging $20

1. How Franklin Templeton thinks about private markets for wealth clients in 2026

Wealth Management Invest podcast, Private Markets and Portfolio Construction w/ Dave Donahoo, head of Americas, Wealth Management Alternatives at Franklin Templeton (Feb 17, 2026)

TLDR:

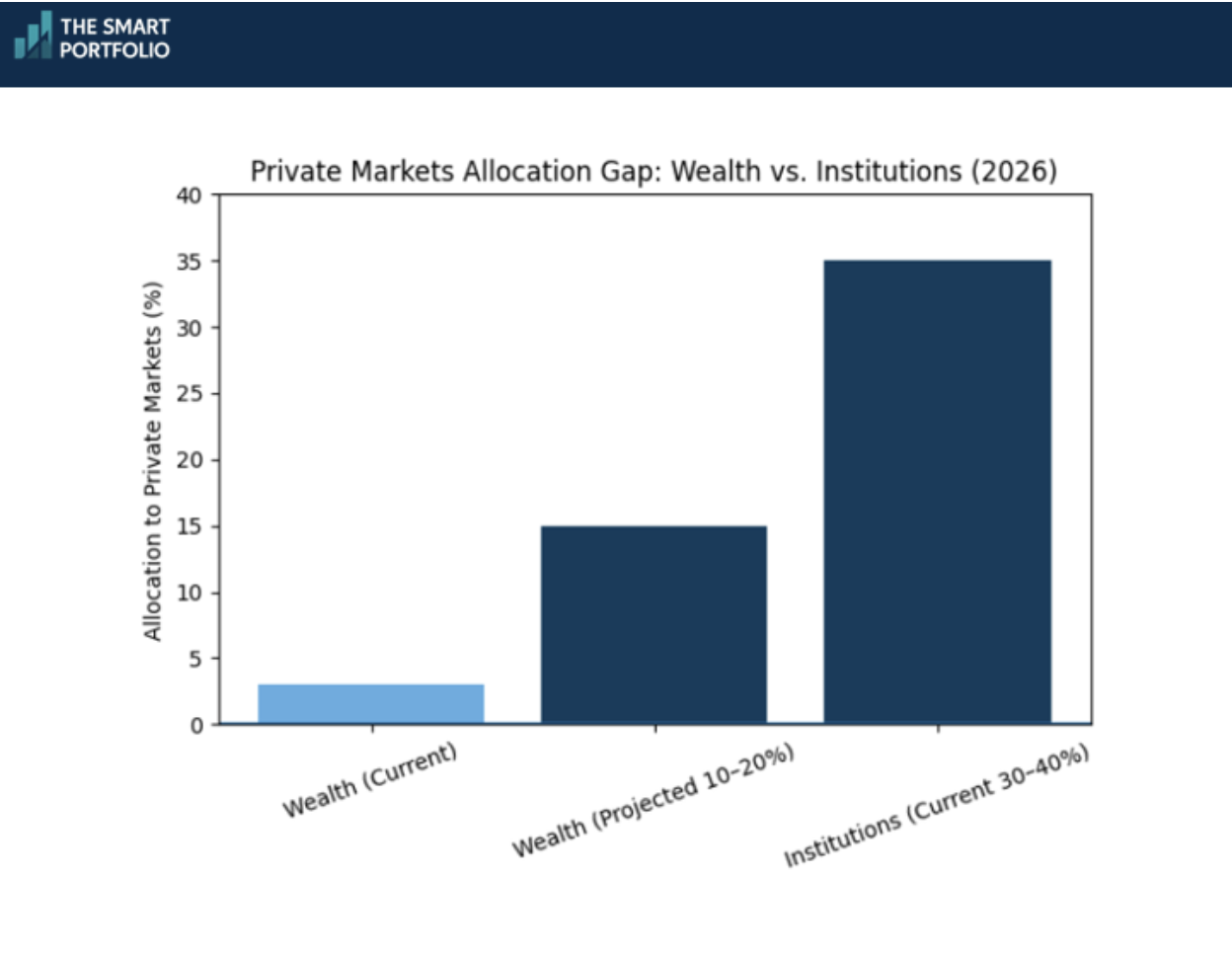

Wealth investors currently allocate roughly 3% to private markets versus 30-40% for institutions. Projections suggest this gap will close to 10-20% over the next decade.

Secondary private equity offers favorable buyer dynamics right now because institutional investors are selling to generate liquidity, creating pricing power for buyers.

Private credit extends far beyond direct lending. Real estate lending currently offers similar yields to direct lending but with better risk-adjusted returns.

Dave Donahoo leads Franklin Templeton's private markets wealth distribution, overseeing a $270 billion business spanning private equity, credit, real estate, and infrastructure. His team of roughly 100 people focuses exclusively on bringing institutional-quality private market solutions to wealth clients.

Why private markets are no longer "alternative"

The statistics make the case compelling: nearly 90% of U.S. companies generating $100 million or more in revenue are privately held. Close to 90% of real estate doesn't trade on exchanges. Direct lending has grown from roughly 5% of total lending after the financial crisis to ~30% today. If you're not investing in private markets, Donahoo argues, you're missing a significant portion of the investable universe.

The key distinction he draws: private markets aren't an alternative asset class anymore. They're core to most portfolios. This shift requires a different conversation with clients, moving from "should we consider alternatives?" to "how do we construct a thoughtful private markets allocation?"

Where the opportunities are in 2026

Secondary private equity stands out for a specific reason: supply and demand favor buyers. Institutional investors who scaled up their commitments during the 2010-2020 period anticipated faster distributions than they're now receiving. With realizations coming back at the slowest pace since 2010, many are selling in the secondary market to generate liquidity. This creates pricing power for secondary buyers who can be highly selective.

Real estate equity presents an early-cycle opportunity. While valuations reset over the past three years due to rising rates, fundamentals in sectors like multifamily and industrial remain strong. The key caveat: office is the exception, not the rule. Office represents roughly 15% of commercial real estate – the other 85% tells a different story.

The private credit nuance advisors miss

Most wealth clients think private credit means direct lending: loans to companies, typically yielding attractive income with NAV stability. But Donahoo emphasizes two other pillars: asset-backed finance and real estate lending.

In upper-market direct lending, so much capital is chasing a finite set of deals that pricing has compressed and covenants have loosened. Real estate lending presents the opposite dynamic: traditional lenders (small and medium banks) are retrenching, creating opportunity for private lenders. The result? Similar yield profiles to direct lending, but with better risk-adjusted positioning.

The bottom line

Building private market allocations requires the same thoughtful approach advisors use for public markets: understanding the difference between private equity and private credit, and the 31 flavors within each.

The website alternativesbyft.com provides educational materials ranging from basic definitions to total portfolio construction frameworks.

2. Email tactics that engage clients: stop educating, your goal is to communicate that you understand your clients on a deeper level

Financial Advisor Marketing podcast: 7 Things My Most Successful Emails Do To Get More Clients (Feb 16, 2026)

TLDR:

The best advisor emails open with client pain points, not education. Readers need to recognize themselves in your communications before they can trust your expertise.

Curiosity beats teaching: if your email fully solves the problem, you've talked too much.

Repelling wrong-fit prospects through clear positioning dramatically improves close rates.

James Pollard analyzed hundreds of emails written specifically for financial advisors to find what separated winners from the rest. His findings challenge conventional wisdom about advisor marketing, especially the instinct to educate prospects into becoming clients.

Start with pain, not information

The best-performing emails don't open with "Here's how to optimize your retirement" or "10 reasons to consider Roth IRAs." Instead, they begin with lines like: "I hear this a lot from people in their 50s..." or "After years of helping physicians plan for retirement, I've noticed something interesting..."

Why does this work? Readers recognize themselves before you explain anything. That recognition builds credibility and bypasses skepticism immediately. Education can come later, after you've earned attention.

Give prospects a way to save face

People who haven't planned well don't want to feel judged. The best emails reframe the problem away from personal failure. Instead of implying someone made bad decisions, position the issue as a gap in the system or a common blind spot. This approach helps prospects feel understood rather than criticized, and that emotional safety makes them far more likely to take action.

One big idea, not a content dump

Winning emails focus on a single organizing concept. Examples include: "Hiring a financial advisor doesn't have to be intimidating," "Not investing is riskier than investing," or "A financial plan is a living document, not a binder on a shelf." Pick one idea. Don't pivot from early retirement to Roth IRAs to HSAs in the same email. Clarity beats comprehensiveness.

Create curiosity, don't teach

Here's the counterintuitive finding: if your email completely solves the reader's problem, you've talked too much. The best emails sharpen the question without fully answering it. They leave readers wanting clarity, not content. That unresolved tension drives appointments.

Repel the wrong people deliberately

An advisor who repels wrong-fit prospects achieves a 40% close rate on 10 appointments (4 clients). An advisor who takes anyone with a pulse hits 20% (2 clients). Same effort, half the result. Make it easy for wrong-fit prospects to self-select out by clearly stating who you don't serve.

The bottom line

Stop trying to educate prospects into becoming clients. Your emails should make readers feel understood, create curiosity about how you can help, and clearly signal who you're not for.

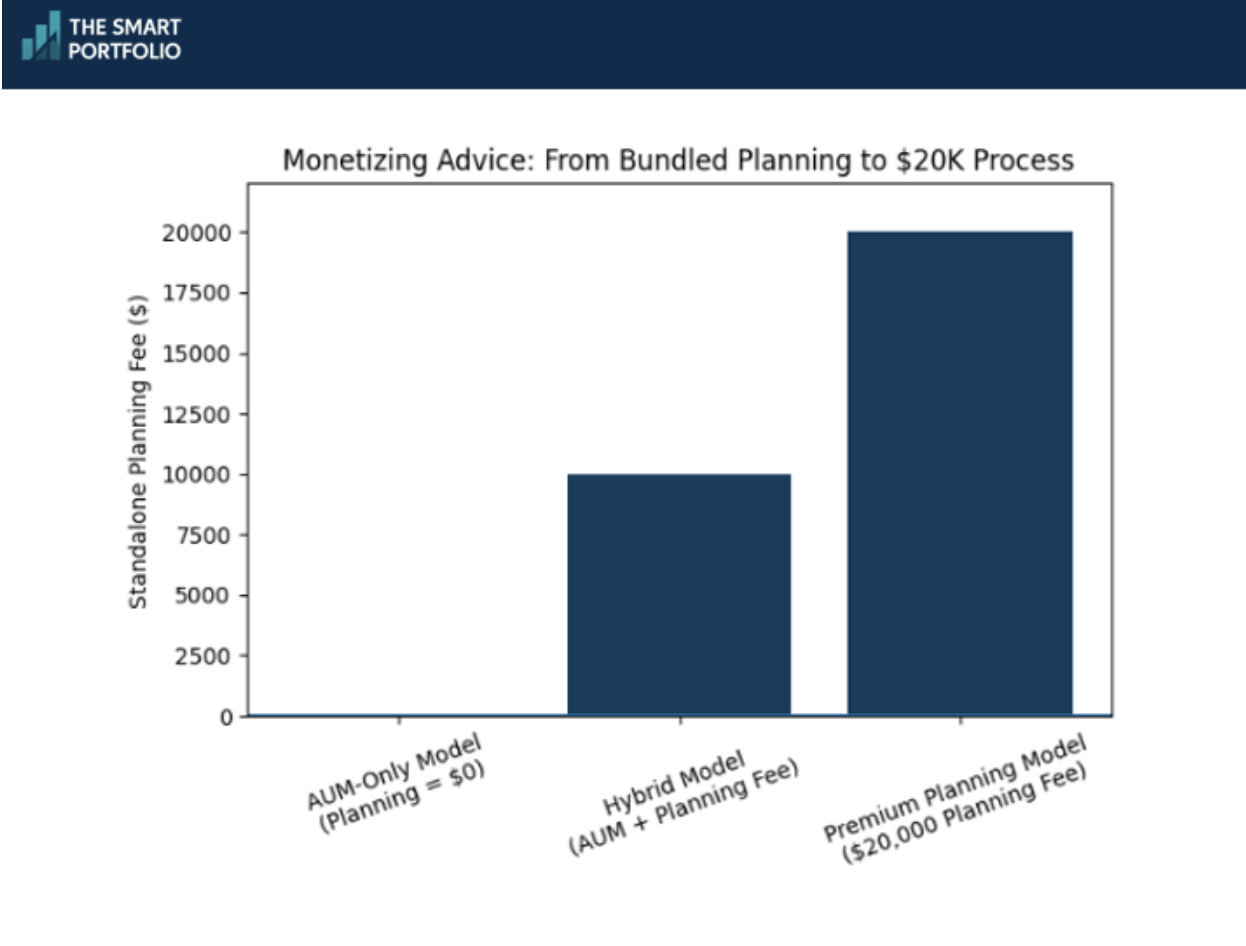

3. This advisor started charging $20,000 for financial planning (and why clients said yes)

The Elite Financial Advisor podcast, $20,000 for Planning: The Process That Changed Everything w/ Mark Hansen (Feb 20, 2026)

TLDR:

Financial advisors can command premium fees by positioning their expertise as a defined planning process, not just investment management.

The shift from AUM-only to charging for advice requires borrowing confidence from peers until you build your own track record.

Clients respond to structured, step-by-step processes that make complex decisions feel manageable.

Mark Hansen didn't set out to charge $20,000 for financial planning. He started like many advisors, managing portfolios and giving away his ideas for free. But after joining the Elite Advisor Network and attending live coaching events, something clicked. He realized the future of advisory isn't just managing money. It's getting paid for what you actually do: think, advise, and guide.

The mindset shift that made premium fees possible

Hansen's mentor was a successful advisor who gave away planning for free. It worked for him after 30 years in the business. But Hansen recognized that approach wouldn't work for someone building a practice from scratch. When he first heard about charging separately for planning, the idea "sank in so deep so fast."

The challenge? He had zero confidence. No one had ever paid him for his ideas alone. At a coaching event, he told a mentor, "I have nothing to lean on." The response was simple: "Then borrow ours." Hansen spent 2025 operating on borrowed confidence, acting as if the model worked because people he trusted said it did. By year's end, he'd collected multiple $20,000 planning fees and built his own proof.

What made clients willing to pay

Hansen developed what he calls the "Clarity Planning Process," a step-by-step framework covering not just investments, but estate planning, protection needs, retirement timelines, and decision sequencing. Instead of overwhelming clients with information, he walks them through each phase methodically.

The key insight: clients appreciate structure. When someone faces 10 possible options, helping them narrow to the two that matter most right now creates enormous value. That's worth paying for.

The entrepreneurship metaphor that keeps him going

Hansen describes his breakthrough using a vivid image: walking downtown on a windy day, sheltered by a building. Entrepreneurship means turning the corner and facing the wind. "Some people don't like to walk into the wind," he says. The advisors who charge premium fees are the ones willing to face that resistance.

The bottom line

If you're giving away comprehensive planning for free while charging only on AUM, you're leaving money on the table, and underselling your expertise. The advisors commanding premium fees have one thing in common: a structured process they can articulate clearly. Start by defining your process, give it a name, and test charging for it. You might be surprised what clients will pay when you stop bundling your best thinking for free.

Disclaimer

This newsletter is for informational and educational purposes only and should not be construed as personalized financial, tax, legal, or investment advice. The strategies and opinions discussed may not be suitable for your individual circumstances. Always consult a qualified financial advisor, tax professional, or attorney before making any decisions that could affect your finances. While we strive for accuracy, we make no representations or warranties about the completeness or reliability of the information provided. Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal. The publisher, authors, and affiliated parties expressly disclaim any liability for actions taken or not taken based on the contents of this publication.